Opinion

By Bashorun J.K. Randle

THE retired partners of KPMG who are still awaiting their pension and gratuity had assembled in Oxford, Oxfordshire, England to reflect on the state of the accountancy profession, which they have been doing for the past twenty years.

Our host, Professor Kenneth Braistow and his charming wife Claire, had made excellent arrangements. However, Professor Braistow was eager to ensure that matters were not confined to accountancy but would rather be broadened to accommodate the principles of politics, philosophy, history and economics.

Matters were not helped by the interjection from Claire that Dr. Nelson Mandela was her choice for our research project – especially what Nigeria has done for South Africa. She proceeded to share the following video by a South African lady.

“Nigeria spent U.S.$61 billion”

During the apartheid era in South Africa, Nigeria played a very prominent role by fully supporting the anti-apartheid movements, including the African National Congress (ANC), which eventually led to dismantling the apartheid regime. Mawuna Remarque Koutonin, narrates the crucial roles Nigeria had played in the struggle against apartheid in South Africa and the liberation of the country after more than 100 years in the apartheid regime`s jaw.

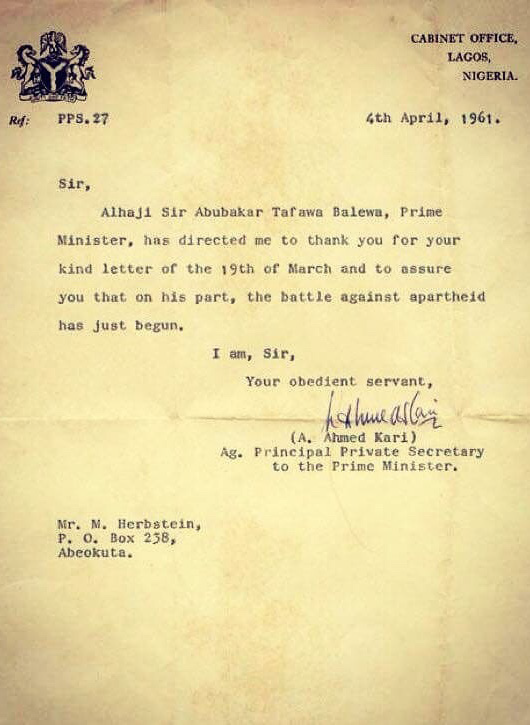

In March 1960, 69 black people were massacred in Sharpeville, South Africa, by the white apartheid police. That same year, Nigeria successfully liberated itself from 160-years British occupation.

The new Nigeria`s leaders` reaction to the Sharpeville massacre has changed everything in South Africa from then on. Here is a letter the then Nigeria`s Prime Minister Abubakar Tafawa Balewa sent to the African National Congress (ANC) “militants“ on April 4, 1961.

Immediately after sending the letter, Sir Balewa lobbied for the effective expulsion of South Africa from the Commonwealth in 1961.

Beyond political support, Sir Abubakar Tafawa Balewa was the first leader to provide a direct financial aid to the ANC from the early 1960s. At the height of the liberation movement in the 1970s, Nigeria alone provided $5-million annual subvention to the ANC and the Pan Africanist Congress (PAC) annually. That amount would be in the billions if converted at today`s rate.

In 1976, Nigeria set up the Southern Africa Relief Fund (SAFR) destined to bring relief to the victims of the apartheid regime in South Africa, provide educational opportunities for them and promote their general welfare.

The successive administrations in Nigeria did not abandon the cornerstone of their country`s foreign policy either. The military administration of General Obasanjo contributed $3.7 million to the fund. Moreover, General Obasanjo made a personal donation of $3,000, while each member of his cabinet also made personal contributions of $1,500 each. All Nigeria`s civil servants and public officers made a 2% donation from their monthly salary to the SAFR. Students skipped their lunch to make donations, and just in 6 months, in June 1977, the popular contribution to the fund reached $10.5 million.

The donations to the SAFR were widely known in Nigeria as the “Mandela tax“.

As a result of the fund`s work, a first group of 86 South African students arrived in Nigeria in 1976, following the disruption of the education system in South Africa. It happened after the massacre of 700 students by the white police while the former were protesting against the decision by the apartheid regime to change their educational language to Afrikaans.

Hundreds of South African students have benefited from the fund`s activity having come to study in Nigeria for free.

Beyond welcoming students and exiles, Nigeria had also welcomed many renowned South Africans like Thabo Mbeki (former South African president from 1999 to 2008). He had spent 7 years in Nigeria, from 1977 to 1984, before he left to the ANC headquarters in Lusaka, Zambia.

For South Africans, who could not travel abroad because the apartheid regime had withdrawn their passports, Nigeria`s government issued more than 300 passports.”

From the archives:

The donations to the SAFR were widely known in Nigeria as the “Mandela tax”. As a result of the fund’s work, a first group of 86 South African students arrived in Nigeria in 1976, following the disruption of the education system in South Africa. It happened after the massacre of 700 students by the white police while the former were protesting against the decision by the apartheid regime to change their education language to Afrikaans.

Students skipped their lunch to make donations, and just in 6 months, in June 1977, the popular contribution to the fund reached $10.5 million.

The donations to the SAFR were widely known in Nigeria as the “Mandela tax”. As a result of the fund’s work, a first group of 86 South African students arrived in Nigeria in 1976, following the disruption of the education system in South Africa. It happened after the massacre of 700 students by the white police while the former were protesting against the decision by the apartheid regime to change their education language to Afrikaans.

Hundreds of South African students have benefited from the fund’s activity having come to study in Nigeria for free. Beyond welcoming students and exiles, Nigeria had also welcomed many renowned South Africans like Thabo Mbeki (former South African president from 1999 to 2008). He had spent 7 years in Nigeria, from 1977 to 1984, before he left to the ANC headquarters in Lusaka, Zambia.

For South Africans, who could not travel abroad because the apartheid regime had withdrawn their passports, Nigeria’s government issued more than 300 passports. Along with fellow African countries Nigeria lobbied for the creation of the United Nations Special Committee against Apartheid and chaired it for 30 years, longer than any other country. Between 1973 and 1978, Nigeria contributed $39,040 to the UN Educational and Training Programme for Southern Africa, a voluntary trust fund promoting education of the black South African elite.

As for trade, Nigeria had refused to sell oil to South Africa for decades in protest against the white minority rule. Nigeria had lost approximately $41 billion during that period. Above all, Nigeria was the only nation worldwide to set up the National Committee Against Apartheid (NACAP) as early as in 1960. The committee’s mission was to disseminate the evils of the apartheid regime to all Nigerians from primary schools to universities, in public media and in markets, through posters and billboards messages. The NACAP was also responsible for the coordination of Nigeria’s government and civil society joint anti-apartheid actions and advising of policy makers on anti-apartheid decisions.

For over three decades the NACAP had successfully built alliances with labor movement, student groups, progressive elements and other international grassroots organizations within Nigeria for effective anti-apartheid activities. In fact, until 1960s, the ANC fight against the apartheid regime in South Africa was yielding very small results. The whole world was quite indifferent to the suffering of the black South Africans. Moreover, western countries strongly supported the apartheid regime providing it with technologies, intelligence and favorable trade agreements. Things started changing dramatically only after African countries became independent in the 1960s.

Nigeria unequivocally took over leadership of the anti-apartheid movement worldwide. Despite the volatile nature of Nigeria’s politics and the passage of numerous military and civil leaders, Nigeria has never abandoned its unwavering commitment to the freedom of our brothers and sisters in South Africa. From 1960 to 1995, Nigeria has alone spent over $61 billion to support the end of apartheid, more than any other country in the world, according to the South African Institute of International Affairs.

The country has never let go of any opportunity to denounce apartheid, from the boycott of Olympic Games and Commonwealth Games to the nationalization of British Petroleum assets in 1979.

Unfortunately, our brothers and sisters in South Africa have not been grateful to Nigeria. When Mandela passed away in 2013, Nigeria’s president was not even given the opportunity to speak. At the same time, the representatives of the US and the UK, two countries supporting the apartheid regime, were in the spotlight. Nigerians still need visas to travel to South Africa, while the French, who used to back the apartheid regime, can just buy a ticket and go wherever they want.

Maybe, apartheid has not yet ended in South Africa.

There is something wonderful about finding out things one did not know about Afrika’s history. Gems like this fund that Nigeria created I only learnt about in January 2022. Imagine that. After all these years on earth, I had my childlike wonder moment when I heard about this great initiative. Yes, it is disappointing that I did not know about it sooner, because it means that this great piece of our history somehow slipped through the cracks and was obviously not given the prominence it has deserved by our governments or educational system… but now that I know about it, it has ignited a new spark of hope in my heart.

In March 1960, 69 black people were massacred in Sharpeville, South Africa, by the white apartheid police. That same year, Nigeria successfully liberated itself from 160-year British occupation. The new Nigeria’s leaders’ reaction to the Sharpeville massacre has changed everything in South Africa from then on. Here is a letter Nigeria’s Prime Minister Abubakar Tafawa Balewa sent to the African National Congress (ANC) militants on April 4, 1961.

Hundreds of South African students have benefited from the fund’s activity having come to study in Nigeria for free. Beyond welcoming students and exiles, Nigeria had also welcomed many renowned South Africans like Thabo Mbeki (former South African president from 1999 to 2008). He had spent 7 years in Nigeria, from 1977 to 1984, before he left to the ANC headquarters in Lusaka, Zambia.

For South Africans, who could not travel abroad because the apartheid regime had withdrawn their passports, Nigeria’s government issued more than 300 passports. Along with fellow African countries Nigeria lobbied for the creation of the United Nations Special Committee against Apartheid and chaired it for 30 years, longer than any other country. Between 1973 and 1978, Nigeria contributed $39,040 to the UN Educational and Training Programme for Southern Africa, a voluntary trust fund promoting education of the black South African elite.

As for trade, Nigeria had refused to sell oil to South Africa for decades in protest against the white minority rule. Nigeria had lost approximately $41 billion during that period. Above all, Nigeria was the only nation worldwide to set up the National Committee Against Apartheid (NACAP) as early as in 1960. The committee’s mission was to disseminate the evils of the apartheid regime to all Nigerians from primary schools to universities, in public media and in markets, through posters and billboards messages. The NACAP was also responsible for the coordination of Nigeria’s government and civil society joint anti-apartheid actions and advising of policy makers on anti-apartheid decisions.

For over three decades the NACAP had successfully built alliances with labor movement, student groups, progressive elements and other international grassroots organizations within Nigeria for effective anti-apartheid activities. In fact, until 1960s, the ANC fight against the apartheid regime in South Africa was yielding very small results. The whole world was quite indifferent to the suffering of the black South Africans. Moreover, western countries strongly supported the apartheid regime providing it with technologies, intelligence and favorable trade agreements. Things started changing dramatically only after African countries became independent in the 1960s.

Nigeria unequivocally took over leadership of the anti-apartheid movement worldwide. Despite the volatile nature of Nigeria’s politics and the passage of numerous military and civil leaders, Nigeria has never abandoned its unwavering commitment to the freedom of our brothers and sisters in South Africa. From 1960 to 1995, Nigeria has alone spent over $61 billion to support the end of apartheid, more than any other country in the world, according to the South African Institute of International Affairs.

The country has never let go of any opportunity to denounce apartheid, from the boycott of Olympic Games and Commonwealth Games to the nationalization of British Petroleum assets in 1979.

Unfortunately, our brothers and sisters in South Africa have not been grateful to Nigeria. When Mandela passed away in 2013, Nigeria’s president was not even given the opportunity to speak. At the same time, the representatives of the US and the UK, two countries supporting the apartheid regime, were in the spotlight. Nigerians still need visas to travel to South Africa, while the French, who used to back the apartheid regime, can just buy a ticket and go wherever they want.

Maybe, apartheid has not yet ended in South Africa.”

It means that we are without excuse.

It means that you and I, my Afrikan brother and sister, must now sit down together at our communal table and plan together all the beautiful things that we have dreamed and envisioned for our Afrika to rise up and become all that she can be!

The fund reached U.S.$10.5 million.”

It was while we were still engaged in intense debate over iconic Dr. Nelson Mandela and the amazing legacy he bequeathed to not only South Africa but the entire world that the Body of Past Presidents (BOPP) of the Institute of Chartered Accountants in Nigeria [ICAN] conveyed by Zoom a request that I deliver the maiden Akintola William Memorial Lecture on 4th September 2004 at the MUSON Centre, Onikan Lagos. What an amazing co-incidence!!

When I relayed the invitation to the other retired partners of KPMG who are still awaiting their gratuity and pension, you could hear the drop of a pin. The profound silence was rapidly replaced by a cacophony of voices advocating immediate acceptance versus those who insisted we should break for lunch and reconvene afterwards for further deliberation on the matter.

Late Mr. Akintola Williams was Doyen of the accountancy profession in Nigeria.

Chief Akintola Williams (9 August 1919 – 11 September 2023) was a Nigerian accountant. He was the first Nigerian to qualify as a chartered accountant.

Williams began his education at Olowogbowo Methodist Primary School, Bankole street, Apongbon, Lagos Island, Lagos, in the early 1930s; the same primary school his late junior brother Chief Rotimi Williams attended. His youngest brother Rev. James Kehinde Williams was a pastor in the same church, Olowogbowo Methodist Church.

His firm founded in 1952, later grew organically and through mergers to become the largest professional services firm in Nigeria by 2004.[2] Williams participated in founding the Nigerian Stock Exchange and the Institute of Chartered Accountants of Nigeria. During a long career, he received many honours.

He married Mabel Efunroye Williams (née Coker) who was a member of the Coker family, a very prominent and influential family in Nigeria. Akintola Williams’ brother-in-law, Mr. F.C.O. Coker, along with Williams helped create the Institute of Chartered Accountants of Nigeria (ICAN) with Williams and Coker being the first and second presidents of ICAN respectively.

Akintola Williams was born on 9 August 1919. His grandfather, Z. A. Williams, was a merchant prince from Abeokuta and his father Thomas Ekundayo Williams was a clerk in the colonial service who set up a legal practice in Lagos after training in London, England. He was the older brother of Frederick Rotimi Williams, who later became a distinguished lawyer, and the late Rev. James Kehinde Williams, a Christian minister. For his primary education in the early 1930s, he attended Olowogbowo Methodist Primary School, Lagos. Williams then attended the CMS Grammar School, Lagos. He went on to Yaba Higher College on a UAC scholarship, obtaining a diploma in commerce. In 1944, he travelled to England where he studied at the University of London. Studying Banking and Finance, he graduated in 1946 with a Bachelor of Commerce. He continued his studies and qualified as a chartered accountant in England in 1949. A Yoruba of chiefly background, the Oloye Williams was one of the founders of the Egbe Omo Oduduwa society while in London, with Dr. Oni Akerele as president and Chief Obafemi Awolowo as Secretary.

After returning to Nigeria in 1950, Williams served with the Inland Revenue as an assessment officer until March 1952, when he left the civil service and founded Akintola Williams & Co. in Lagos. The company was the first indigenous chartered accounting firm in Africa. At the time, the accountancy business was dominated by five large foreign firms. Although there were a few small local firms, they were certified rather than chartered accountants. Williams gained business from indigenous companies including Nnamdi Azikiwe‘s West African Pilot, K. O. Mbadiwe‘s African Insurance Company, Fawehinmi Furniture and Ojukwu Transport. He also provided services to the new state-owned corporations including the Electricity Corporation of Nigeria, the Western Nigeria Development Corporation, the Eastern Nigeria Development Corporation, the Nigerian Railway Corporation and the Nigerian Ports Authority.

The first partner in the firm, Charles S. Sankey, was appointed in 1957, followed by the Cameroonian Mr. Njoh Litumbe. Litumbe opened branch offices in Port Harcourt and Enugu, and later spearheaded overseas expansion. In 1964, a branch was opened in the Cameroons, followed by branches in Côte d’Ivoire and Swaziland, and affiliates in Ghana, Egypt and Kenya. By March 1992, the company had 19 partners and 535 staff.

Demand grew as a result of the Companies Act of 1968, which required that companies operating in Nigeria formed locally incorporated subsidiaries and published audited annual accounts. The drive in the early 1970s to encourage indigenous ownership of businesses also increased demand. In 1973, AW Consultants Ltd, a management consultancy headed by Chief Arthur Mbanefo, was spun off. The company acquired a computer service company and a secretarial service, and in 1977, the company entered into an agreement with Touche Ross International based on profit sharing. Williams was also a board member and major shareholder in a number of other companies. He retired in 1983.

Between April 1999 and May 2004, Akintola Williams & Co. merged with two other accounting firms to create Akintola Williams Deloitte (now known as Deloitte & Touche), the largest professional services firm in Nigeria with a staff of over 600.

Williams played a leading role in establishing the Association of Accountants in Nigeria in 1960 with the goal of training accountants. He was the first President of the association. He was founding member of the Institute of Chartered Accountants of Nigeria. He was also involved in establishing the Nigerian Stock Exchange. He remained actively involved with these organisations into his old age. At a stock exchange ceremony in May 2011, he called on operators to protect the market and ensure there was no scandal. He said that, if needed, market operators should not hesitate to seek his advice on resolving any problem.

Public sector positions held by him include Chairman of the Federal Income Tax Appeal Commissioners (1958–68), member of the Coker Commission of Inquiry run by his brother-in-law Justice G.B.A. Coker, a Lagos High Chief, into the Statutory Corporations of the former Western Region of Nigeria (1962), member of the board of Trustees of the Commonwealth Foundation (1966–1975), Chairman of the Lagos State Government Revenue Collection Panel (1973) and Chairman of the Public Service Review Panel to correct the anomalies in the Udoji Salary Review Commission (1975). Other positions include President of the Metropolitan Club in Victoria Island, Lagos, Founder and Council member of the Nigerian Conservation Foundation and Founder and chairman of the board of Trustees of the Musical Society of Nigeria.

In 1982, Williams was honoured by the Nigerian Government with the O.F. R. Following retirement in 1983, Williams threw himself into a project to establish a music centre and concert hall for the Music Society of Nigeria. In April 1997, Williams was appointed a Commander of the Most Excellent Order of the British Empire for services to the accountancy profession and for promotion of arts, culture and music through the Musical Society of Nigeria. The Akintola Williams Arboretum at the Nigerian Conservation Foundation headquarters in Lagos is named in his honour. On 8 May 2011, the Nigeria-Britain Association presented awards to John Kufuor, past President of Ghana, and to Akintola Williams, for their contributions to democracy and development in Africa.

Williams turned 100 in August 2019, and died at his home in Lagos on 11 September 2023, at the age of 104.

The title of the Lecture would be :

“Leadership Dynamics: Current Realities And Way Forward”

When we resumed proceedings after lunch, the argument went back and forth over the choice of topic and the content/focus of the lecture. Thankfully, due to the sagacity (fuelled by plenty of wine and champagne) of the former KPMG partners we arrived at a consensus by the end of the evening.

What was agreed was that the lecture I would deliver would be anchored on research based on empirical evidence that would attempt to beam the searchlight on the current state of the accountancy profession.

The “Financial Times” fired the first salvo:

“PWC Fined £15 million for LCF Audit Failure”

“Big Four firm hit for not alerting watchdog of fraud fears at investment group”

“Britain’s financial regulator fined audit firm PwC 15 million pounds ($19.3 million) on Friday for failing to alert the watchdog that London Capital & Finance (LCF) might be involved in fraudulent activity ahead of its costly collapse for taxpayers.

The fine throws a spotlight on the longstanding debate about how far auditors should be responsible for spotting and flagging potential fraud.

PwC, one of the world’s “Big Four” auditors, encountered “significant issues” through its 2016 audit of LCF, the investment firm that collapsed in early 2019, the Financial Conduct Authority, opens new tab said on Friday.

It left investors facing losses on unregulated ‘mini bonds’ they had bought from LCF, with Britain’s taxpayers having to pay about 120 million pounds to compensate them.

The FCA, which in February banned and fined a former director of LCF, said that a senior individual at LCF “acted aggressively towards auditors”, and the firm provided PwC with “inaccurate and misleading information”.

“LCF’s actions, and PwC’s own work on the audit, led PwC to suspect that LCF might be involved in fraudulent activity. PwC was duty bound to report those suspicions to the FCA as soon as possible, but they failed to do so,” the watchdog said in a statement.

PwC said the FCA has acknowledged that the auditor was not involved in the misconduct at LCF.

“We have reached a settlement with the FCA to resolve an unintentional reporting breach,” PwC said in a statement.

LCF’s collapse led to a damning independent review, opens new tab of the FCA, resulting in an internal shake-up at the watchdog.

Britain’s accounting watchdog, the Financial Reporting Council, opens new tab, has sanctioned fined PwC, along with EY and Oliver Clive & Co following its investigation into the audits of LCF.

The Serious Fraud Office has an open criminal investigation into the failures at LCF.

Following accounting scandals at retailer BHS and builder Carillion, one review, opens new tab said the “gap” between public expectations about auditors’ ability to detect fraud and their responsibility to do so, needed addressing.

The FCA said PwC was not responsible for “seeking out or fully investigating” suspected fraud, but auditors’ “unique insight” into companies means they have an important role in alerting watchdogs.”

Shivaram Rajgopal – Professor at Columbia Business School:

“Why Don’t We Ask Companies And Auditors To Disclose Their Materiality Standards”?

“In today’s column on Forbes, I ask an innocuous question that I had never thought of asking before. We see so much handwringing about “materiality” in financial statements whenever new disclosure rules are discussed or when a disclosure case goes to court. Yet, we never seem to ask firms and auditors to simply tell us what materiality standards they used when they prepared and audited a firm’s financial statements.

This is where travel and exposure to foreign settings helps. Columbia Business School ran a faculty tour of China in early June that I was lucky to be a part of. One of the businesses we visited during that trip was the Chinese electric vehicle giant, BYD. I used to go over the financial statements of any company we visited as a quick way of familiarizing myself with the stated narrative and the proof points of that business. It turns out that BYD clearly discloses the numerical thresholds they use in determining materiality standards in their financial statements. We often think of Chinese financial reporting and governance systems as relatively opaque relative to the ones we have in the West. While that is true in many respects, they also innovate along dimensions that we don’t often think about. Will the Financial Accounting Standards Board , the U.S. Securities and Exchange Commission and the Public Company Accounting Oversight Board (PCAOB) consider asking US managers and auditors to publish their materiality thresholds for individual firms and/or transactions?”

Ernst & Young

“Big four” accountancy firms PricewaterhouseCoopers and EY have been fined a combined £9.3m for a series of failures in auditing the accounts of London Capital & Finance, the collapsed mini-bond firm that wiped out the investments of thousands of savers.

It concludes a near four-year investigation by the Financial Reporting Council (FRC) into how auditors breached their duties while reviewing the firm’s finances in the years leading up to its demise in 2019.

Jamie Symington, the regulator’s deputy executive counsel, said the auditors failed to understand the business and raised the possibility that there could be “material misstatements” in the company’s accounts.

“These breaches are made considerably more serious by the fact that all of the auditors knew they were auditing an expanding business which was engaged in selling unregulated financial products to retail investors, and that potential investors might place reliance on the clean audit opinions,” Symington said.

London Capital & Finance (LC&F) collapsed in 2019, after taking about £237m from 11,600 investors. Its mini-bonds promised stellar returns of up to 8% a year, but put only a small amount of cash into safe interest-bearing investments.

The rest was funnelled into speculative property developments, oil exploration in the Faroe Islands and even a helicopter bought for a company controlled by LC&F. The company collapsed in January 2019. The scandal has led to reprimands for the City regulator, the Financial Conduct Authority, and prompted a criminal investigation by the Serious Fraud Office, which is still open.

PricewaterhouseCoopers (PwC) and one of its staff members – who were appointed as auditors for the 2016 financial year – admitted to eight breaches, the most serious being a failure to adequately understand the nature of LC&F’s business and internal controls.

That year, the firm issued £9.2m in bonds and was growing even more rapidly by the time the audit report was signed, the regulator said. However, PwC did not apply “sufficient professional scepticism” while conducting its audit, the FRC said.

EY took over as LC&F’s auditor for the 2017 financial year, after PwC resigned. That year, LC&F ramped up its operations, selling a further £53.4m in bonds. But EY fell short, having also failed to understand and properly scrutinise the business, particularly in light of the risk of fraud. EY and one of its employees has since admitted to six breaches of FRC rules.

PwC and EY have been severely reprimanded for their failings and hit with fines worth £4.9m and £4.4m respectively. It marks the largest-ever fine issued against EY by the FRC to date, and the third largest for PwC.

A smaller auditor, Oliver Clive & Co, was fined a further £42,000 in relation to LC&F’s 2015 audit. All three firms cooperated with the regulator, resulting in reduced fines.

“We are sorry our work in 2016 did not meet the standards expected and that we expect of ourselves,” a PwC spokesperson said, adding that the firm had made “significant changes” to its processes and policies over the past eight years.

EY said in a statement that it had fully cooperated with the FRC throughout the investigation. “Our 2017 audit of LC&F fell short of our standards and for this we apologise. We have taken significant steps to address the issues identified and we are committed to learning from our mistakes.”

Oliver Clive & Co was contacted for comment.”

Deloitte fined £900,000 by watchdog over SIG audit failures

Financial sanctions relate to audit of building materials firm’s statements for years 2015 and 2016

Deloitte has been fined more than £900,000 by the accounting watchdog after failures in its audit of the building materials firm SIG.

The Financial Reporting Council (FRC) also handed a fine of £36,250 to Simon Manning, who was the audit engagement partner working on the account.

Deloitte’s initial fine was £1.25m but the sum was discounted after the “big four” accountancy firm admitted the breaches. Manning’s fine was also reduced from £50,000 to £36,250.

Deloitte and Manning admitted to two breaches in relation to the audit of supplier rebates – financial incentives paid by SIG to its suppliers – and cash.

The FRC said that Deloitte failed to obtain enough audit evidence testing the rebate terms and the debtor balances. It also failed to “exercise sufficient professional scepticism” by not investigating indications that rebate debtor balances could have been overstated.

Jamie Symington, deputy executive counsel, said: “These breaches concerned two discrete areas of the audit of a particular subsidiary of SIG plc. They involved contraventions of requirements which are fundamental to the role of the independent auditor, and were associated with material misstatements in SIG plc’s accounts which had to be corrected.

“The breaches in respect of supplier rebates were made all the more serious by the fact that the FRC had highlighted these complex supplier arrangements as requiring particular attention from auditors.”

The financial sanctions were in relation to the audit of financial statements of SIG in the financial years ended 31 December 2015 and 31 December 2016.

A spokesperson for Deloitte said: “We are disappointed that our work on the full-year 15 and full-year 16 SIG plc audits – relating to the audit of supplier rebates and cash – fell short of the high standards expected of us.”

Global: KPMG Faces Historic £21 Million Fine for Carillion Audit Failures

The Financial Reporting Council (FRC) has levied a landmark £21 million fine against KPMG for its audit of Carillion, the government contractor that went under in 2018.

In a statement issued on Thursday, the FRC indicated that while the initial penalty was £30 million, it was subsequently reduced by 30% owing to KPMG’s cooperation during the five-year investigation.

The FRC underscored Carillion’s substantial importance as a client for KPMG, noting that KPMG’s audit team, including key members, faced potential “objectivity risks” due to their association with Carillion.

Jon Holt, CEO and senior partner of KPMG in the UK, expressed, “These findings are severe. We have fully cooperated with the investigation, and we accept its conclusions and the sanctions imposed without reservation. I deeply regret that these shortcomings occurred within our firm.”

The legal action, centering on audits of Carillion’s accounts spanning 2014 to 2016, was instigated by Britain’s official receiver with the aim of recouping losses for Carillion’s creditors.

The FRC’s statement called attention to Peter Meehan, a former partner at KPMG who is no longer with the company. The FRC specified that Meehan, who led the audit, and his team, on occasions, greenlit audit reports before completing all necessary work.

Meehan was subjected to a financial penalty of £500,000, later reduced by 30% to £350,000, acknowledging his cooperation and admissions during the investigation. Additionally, another former KPMG partner, Darren Turner, received a £100,000 fine for his role in the audit.

KPMG’s Holt acknowledged that the firm’s audit work had been “very poor,” and former partners at the company failed to fulfill their duties adequately.

“Junior colleagues were seriously let down by those who should have set a clear example, and I am both saddened and infuriated that this transpired at our firm.”

KPMG and Holt conveyed their inability to defend the work performed on Carillion and have since implemented various enhancements to prevent a recurrence of such failures.

Elizabeth Barrett, executive counsel at the FRC, commented, “Many of the breaches involved the failure to adhere to fundamental audit principles, such as maintaining professional skepticism and acquiring sufficient appropriate audit evidence.”

In response to the Carillion scandal and other high-profile collapses, government ministers had pledged to overhaul the audit and corporate governance systems. However, news emerged in September 2023 that government officials might delay the scheduled revamp of the UK’s audit and governance framework.

The recent fines imposed on KPMG underscore the urgency for the government to publish the Audit Reform Bill, which was promised over a year ago, as stated by Anne Kiem OBE, CEO of the Chartered Institute of Internal Auditors.

“This legislation is urgently needed to establish the audit regulator on a statutory basis, equipped with the requisite legal powers to effectively execute its duties.”

The main thrust of the research is the human angle – what happens to the lives of those who are sucked into the dark vortex of audit failures. Accountancy is already well established as a pressure cooker profession even at the best of times. Success is celebrated with gusto but failure is treated with disdain – slow poison.

In most cases, once a complaint or investigation is launched, the minimum disciplinary action is the garden leave which means you stay away from the office.

“A federal judge vacated fraud convictions for two former KPMG partners after providing similar relief to several of their co-defendants charged with trying to help the Big Four audit firm cheat on its regulatory inspections.”

JEFF STEIN – KPMG : Ministry of Justice

“WASHINGTON, D.C. – KPMG LLP (KPMG) has admitted to criminal wrongdoing and agreed to pay $456 million in fines, restitution, and penalties as part of an agreement to defer prosecution of the firm, the Justice Department and the Internal Revenue Service announced today. In addition to the agreement, nine individuals-including six former KPMG partners and the former deputy chairman of the firm-are being criminally prosecuted in relation to the multi-billion dollar criminal tax fraud conspiracy. As alleged in a series of charging documents unsealed today, the fraud relates to the design, marketing, and implementation of fraudulent tax shelters.

In the largest criminal tax case ever filed, KPMG has admitted that it engaged in a fraud that generated at least $11 billion dollars in phony tax losses which, according to court papers, cost the United States at least $2.5 billion dollars in evaded taxes. In addition to KPMG’s former deputy chairman, the individuals indicted today include two former heads of KPMG’s tax practice and a former tax partner in the New York, NY office of a prominent national law firm.

“Corporate fraud has far-reaching consequences, both to the marketplace and those whose livelihoods depend on companies that maintain honest business practices,” said Attorney General Alberto R. Gonzales. “Today’s agreement requires KPMG to accept responsibility and make amends for its criminal conduct while protecting innocent workers and others from the consequences of a conviction. The stiff financial penalty announced today means that the firm is paying for its conduct, while the guarantees of cooperation, oversight, and meaningful reform will help to ensure that its future business is conducted with honesty and integrity.”

The criminal information and indictment together allege that from 1996 through 2003, KPMG, the nine indicted defendants and others conspired to defraud the IRS by designing, marketing and implementing illegal tax shelters. The charging documents focus on four shelters that the conspirators called FLIP, OPIS, BLIPS and SOS. According to the charges, KPMG, the indicted individuals, and their co-conspirators concocted tax shelter transactions-together with false and fraudulent factual scenarios to support them-and targeted them to wealthy individuals who needed a minimum of $10 or $20 million in tax losses so that they would pay fees that were a percentage of the desired tax loss to KPMG, certain law firms, and others instead of paying billions of dollars in taxes owed to the government. To further the scheme, KPMG, the individual defendants, and their co-conspirators allegedly filed and caused to be filed false and fraudulent tax returns that claimed phony tax losses. KPMG also admitted that its personnel took specific deliberate steps to conceal the existence of the shelters from the IRS by, among other things, failing to register the shelters with the IRS as required by law; fraudulently concealing the shelter losses and income on tax returns; and attempting to hide the shelters using sham attorney-client privilege claims.

The information and indictment allege that top leadership at KPMG made the decision to approve and participate in shelters and issue KPMG opinion letters despite significant warnings from KPMG tax experts and others throughout the development of the shelters and at critical junctures that the shelters were close to frivolous and would not withstand IRS scrutiny;

that the representations required to made by the wealthy individuals were not credible; and the consequences of going forward with the shelters-as well as failing to register them-could include criminal investigation, among other things.

The agreement provides that prosecution of the criminal charge against KPMG will be deferred until December 31, 2006 if specified conditions-including payment of the $456 million in fines, restitution, and penalties-are met. The $456 million penalty includes: $100 million in civil fines for failure to register the tax shelters with the IRS; $128 million in criminal fines representing disgorgement of fees earned by KPMG on the four shelters; and $228 million in criminal restitution representing lost taxes to the IRS as a result of KPMG’s intransigence in turning over documents and information to the IRS that caused the statute of limitations to run. If KPMG has fully complied with all the terms of the deferred prosecution agreement at the end of the deferral period, the government will dismiss the criminal information.

To date, the IRS has collected more than $3.7 billion from taxpayers who voluntarily participated in a parallel civil global settlement initiative called Son of Boss. The BLIPS and SOS shelters are part of the Son of Boss family of tax shelters.

The agreement requires permanent restrictions on KPMG’s tax practice, including the termination of two practice areas, one of which provides tax advice to wealthy individuals; and permanent adherence to higher tax practice standards regarding the issuance of certain tax opinions and the preparation of tax returns. In addition, the agreement bans KPMG’s involvement with any pre-packaged tax products and restricts KPMG’s acceptance of fees not based on hourly rates. The agreement also requires KPMG to implement and maintain an effective compliance and ethics program; to install an independent, government-appointed monitor who will oversee KPMG’s compliance with the deferred prosecution agreement for a three-year period; and its full and truthful cooperation in the pending criminal investigation, including the voluntary provision of information and documents.

Richard Breeden, former Securities and Exchange Commission Chairman, has been appointed to serve as the independent monitor. After his duties end, the IRS will monitor KPMG’s tax practice and adherence to elevated standards for two years.

Should KPMG violate the agreement, it may be prosecuted for the charged conspiracy, or the government may extend the period of deferral and/or the monitorship.

“Today’s actions demonstrate our resolve to hold accountable those who play fast and loose with the tax code,” said IRS Commissioner Mark Everson. “At some point such conduct passes from clever accounting and lawyering to theft from the people. We simply can’t tolerate flagrant abuse of the law and of professional obligations by tax practitioners, particularly those associated with so-called blue chip firms like KPMG, that by virtue of their prominence set the standard of conduct for others. Accountants and attorneys should be the pillars of our system of taxation, not the architects of its circumvention.”

The nine individuals named in the indictment are:

- Jeffrey Stein, former Deputy Chairman of KPMG, former Vice Chairman of KPMG in charge of Tax, and former KPMG tax partner;

- John Lanning, former Vice Chairman of KPMG in charge of Tax, and former KPMG tax partner;

- Richard Smith, former Vice Chairman of KPMG in charge of Tax, a former leader of KPMG’s Washington National Tax, and former KPMG tax partner;

- Jeffrey Eischeid, former head of KPMG’s Innovative Strategies group and its Personal Financial Planning Group, and former KPMG tax partner;

- Philip Wiesner, former Partner-In-Charge of KPMG’s Washington National Tax office and former KPMG tax partner;

- John Larson, a former KPMG senior tax manager;

- Robert Pfaff, a former KPMG tax partner;

- Raymond J. Ruble, a former tax partner in the New York, NY office of a prominent national law firm; and

- Mark Watson, a former KPMG tax partner in its Washington National Tax office.

The indictment alleges that as part of the conspiracy to defraud the United States, KPMG, the nine defendants and their co-conspirators prepared false and fraudulent documents- including engagement letters, transactional documents, representation letters, and opinion letters-to deceive the IRS if it should learn of the transactions. KPMG, the indicted defendants and their co-conspirators are also charged with preparing false and fraudulent representations that clients were required to make in order to obtain opinion letters from KPMG and law firms-including Ruble’s law firm-that purported to justify using the phony tax shelter losses to offset income or gain. The conspirators allegedly concealed from the IRS the fact that the opinion letters provided by KPMG and the law firms were not independent and were instead prepared by entities involved in the design, marketing and implementation of the shelters. Had the IRS known this, the opinion letters would have been rendered worthless.

KPMG admitted that the opinion letters issued for the FLIP, OPIS, BLIPS and SOS shelters were false and fraudulent in numerous respects, including false claims that transactions were legitimate investments instead of tax shelters; and also false claims that clients were entering into certain transactions making up the shelters for investment purposes or to diversify their portfolios, when these actually served to disguise the shelters. KPMG also admitted that the clients’ motivations were to get a tax loss, and with respect to BLIPS, the opinion letters also included false claims about the duration of the transaction and the clients’ motivation for terminating the transaction. According to the charges, BLIPS was also based on false claims about the existence and investment purpose of a loan, when these were in fact sham loans that had nothing to do with any investment, and at least one of the banks never even funded the purported loans.

According to the charging documents, Smith, Eischeid, and others caused KPMG to provide false, misleading and incomplete documents and testimony in response to a Senate subpoena, which was delivered as part of an investigation into tax shelters being conducted by the Senate Governmental Affairs Committee’s Permanent Subcommittee on Investigations.

Assistant U.S. Attorneys Justin S. Weddle and Stanley J. Okula, Jr.-together with Special Assistant U.S. Attorney and Tax Division Trial Attorney Kevin M. Downing-are in charge of the prosecution. The investigation and prosecution are being supervised by Shirah Neiman, Chief Counsel to the U.S. Attorney for the Southern District of New York. For the IRS, the case was investigated by a team of special agents and revenue agents from the agency’s criminal and civil divisions.

The individual defendants are scheduled to be arraigned by Judge Lewis Kaplan.

The charges contained in the indictment are merely accusations, and the defendants are presumed innocent unless and until proven guilty.”

The KPMG tax shelter fraud scandal involved illegal U.S. tax shelters by KPMG that were exposed beginning in 2003. In early 2005, the United States member firm of KPMG International, KPMG LLP, was accused by the United States Department of Justice of fraud in marketing abusive tax shelters.

Tax shelters are any method of reducing taxable income resulting in a reduction of the payments to tax collecting entities, including state and federal governments.[1] The methodology can vary depending on local and international tax laws.

SUICIDE RATES

TOP 10 JOBS WITH HIGHEST SUICIDE RATES

Year after year National Institute for Occupational Safety & Health (NIOSH) compiles the list of jobs with highest suicide rates.

Money seems to be one of the main struggles. Money makes the world go ’round. Working to earn enough money to survive, or maintain a lifestyle, however luxurious or not, is a source of daily struggle for everyone.

Almost every job has some sort of level of stress. There are number of things that can create employment nerve-wracking are unreasonable client demands, long hours and the emotional trauma that comes with it. Most of the people will find ways to manage and overcome stress. However, some are unable to cope with the stress of the job.

According to Mental Health Daily:

Year after year, both dentists and doctors remain among the occupations with the highest suicide rates. It seems as though in the United States, jobs requiring significant levels of aptitude, sacrifice, and education seem to be those with above-average risk of suicide. Oddly enough, contrasting evidence has emerged in countries like Britain that indicates the opposite trend to be true: occupations requiring lower skill tend to carry increased rates of suicide.

SO WHAT ARE THE JOBS WITH HIGHEST SUICIDE RATES?

1.Medical Doctors

2. Dentists

3. Police Officers

4. Veterinarians

5. Financial Services

6. Real Estate Agents

7. Electricians

8. Lawyers

9. Farmers

10. Pharmacists.

The lawyers are called in and that is when the drama takes an entirely different direction. There is never any time limit. Hence, the ordeal could go on for weeks, months or even years. This requires diligent research with would rely on case studies. The mental anguish is truly monumental. Apparently, there are many victims who have provided well detailed testimony of the devastation inflicted on them. Mind you some of them are thoroughly guilty of negligence. They failed in their duty of care. Others are innocent victims of circumstances beyond their control. In any case, poor judgement is never accepted as an excuse. Indeed, it is a murky world where descent into depression and other psychological problems sometimes result in suicide. There are no prizes for blunders. We are dealing with the very dark side of the accountancy profession.

According to Professor James Hanson, his research is driven by data accumulated over six decades – going back to the collapse of Arthur Andersen over its handling of Enron.

A rather strange dimension is provided by the suggestion that alcoholism and drugs cannot be ruled out entirely.

It is also very rare for offenders or victims to be given a chance to atone for past mistakes.

The question that must be addressed is: who cares about the mental health of auditors ? They sometimes work under extreme pressure and fatigue to meet deadlines. Isolation is a factor made more cruel by working in a team where espirit de corps subsumes everything else.

What emerges is that Chartered Accountants are not insulated from marital problems which could seriously impair their judgement and undermine the quality of their work.

It is a throwback into the realm of uncertainties and probabilities that remind us of Thomas Bayes, the 18th century Presbyterian who was obsessed with using statistics to probe the mind of God.

So where are the statistics that would capture the Chartered Accountants who have fallen right through the comfort zone and safety net to the dungeons of poverty, homelessness and hopelessness just because they signed off on the wrong figures and accounts ?

Perhaps nobody cares anyway. There are always going to be losers and winners.

SERIOUS FRAUD

OFFICE

On Monday 2nd September 2024, Interim Chief Capability Officer Freya Grimwood delivered a keynote speech at the Cambridge International Symposium on Economic Crime.

The Serious Fraud Office (SFO) has today charged Alex Beard, Andrew Gibson, Paul Hopkirk, Ramon Labiaga and Martin Wakefield with conspiring to make corrupt payments in order to benefit commodities giant Glencore’s oil operations in West Africa.

The Serious Fraud Office (SFO) is a non-ministerial government department of the Government of the United Kingdom that investigates and prosecutes serious or complex fraud and corruption in England, Wales and Northern Ireland. The SFO is accountable to the Attorney General for England and Wales, and was established by the Criminal Justice Act 1987, an Act of the Parliament of the United Kingdom.

Section 2 of the Criminal Justice Act 1987 grants the SFO powers to require any person (or business/bank) to provide any relevant documents (including confidential ones) and answer any relevant questions including ones about confidential matters. The SFO is the principal enforcer of the Bribery Act 2010, which has been designed to encourage good corporate governance and enhance the reputation of the City of London and the UK as a safe place to do business. Its jurisdiction does not extend to Scotland, where fraud and corruption are investigated by Police Scotland through their Specialist Crime Division, and prosecutions are undertaken by the Economic Crime Unit of the Crown Office and Procurator Fiscal Service.

A.I

Sept. 19, 2024

Tags: Bashorun J.K. Randle